Research

10 min read

CESR: Enabling Consistent ETH Staking Returns

Composite Ether Staking Rate (CESR) 101

Published on

September 8, 2024

Introduction

The Composite Ether Staking Rate (CESR) might just be the next biggest innovation in the staking space. While staking and Proof of Stake cryptocurrencies have burgeoned in popularity, interesting developments aims at making them more usable to investors and create a stable form of revenue generation.

CESR is not a technological shift, but more of a financial one. While CESR in and of itself represent a benchmark metric (average APR) that validators have to abide by, the CESR swap structure is a series of agreements that powers a more stable, predictable, and accessible staking experience. This agreement, while simple, has many nuances which we shall explore in this article. But before that, let’s discuss what CESR actually brings to the table for the parties involved.

Clients

Clients served by staking providers are often institutional stakers (VCs, Exchanges, Custodians) who use staking as a form of revenue generation or product offering. However, the major caveat with staking is the variable rate of this revenue, which prevents it from being a reliable periodic source. When operating a business, accounting expenses and payroll require strictly forecastable and regular incoming revenue.

With CESR, clients can set up an agreement with the staking provider to receive a fixed rate staking revenue every month, regardless of market conditions or infrastructure performance considerations. This stability allows businesses to plan their finances more effectively and ensures a reliable income stream.

Validators

A validator, such as Luganodes, typically relies on charging commissions from staking revenue. Since the staking revenue rate is variable, so is the revenue generation for the company. CESR changes this dynamic by enabling validators to provide a fixed rate to clients.

This stability attracts more businesses seeking a reliable revenue stream, bringing more clients into the staking space. Additionally, validators receive stable investments from partner liquidity providers to meet client demands, allowing them to keep an extra cut for further investments or insurance. This creates a new financial setup for validators and boosts the overall confidence in the staking market.

Liquidity Providers

Liquidity providers (LPs) participate in the CESR initiative as investors, fueling the staking economy. Analysts from LPs predict massive potential in the staking space, and CESR gives them early exposure to this ecosystem. In a way, LPs use this as a speculative derivative venture.

By trusting certain validators, LPs build a hedge against future market fluctuations. However, validators must adhere to a market-wide average performance level for LPs to trust their performance. CESR defines this benchmark rate, forming the bedrock of the agreement.

CESR Structure

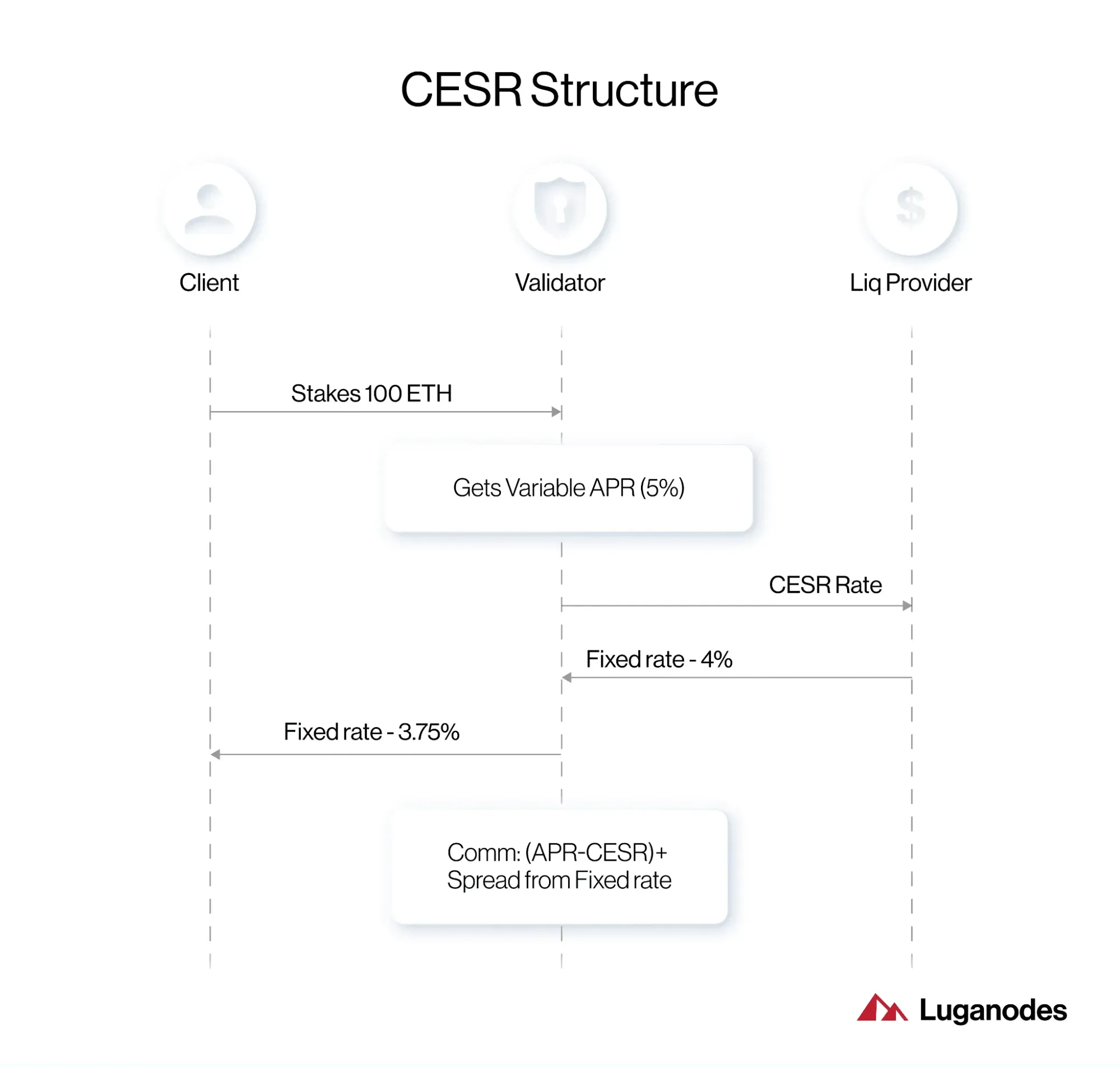

We can now look into the practical execution of CESR, using an example. We shall assume that we have a client, who has staked 100 ETH with our staking service. They expect a return of 1.25 ETH per quarter to meet their expenses and operational costs.

However, a validator in reality would have a fluctuating rate, providing something like 1, 0.25, 1.5, and 1.25 ETH in each of the quarters (example given for illustration, in practice, it will be a lesser spread), and this poses a major problem and issue for others looking forward to getting involved in staking.

Example 1

Analyzing the diagram provided below, we can see the transactions and the steps involved - in a CESR-enhanced system.

The client stakes 100 ETH with the validator. The validator ends up generating a variable APR. For this year, we assume it was 5%, which amounts to 5 ETH.

The client stakes 100 ETH with a validator. The validator generates a variable APR; for this year, we assume it to be 5%, which amounts to 5 ETH.

The validator is bound by two agreements: providing a fixed staking return to the client, which in this example is 3.75%, and maintaining a fixed CESR, governed by the average APR across the market.

A Liquidity Provider offers a fixed 4% to the validator. After keeping a small commission (0.25%), the validator passes the remainder to the client, independent of market or performance conditions.

In this setup, the validator must adhere to the market-wide CESR rate. This incentivizes the validator not only to maximize APR for profit but also to compete with other validators to outperform the market average. This dynamic fosters a more competitive validator market for clients, who benefit from a stable and regular return.

Returning to our example, the client is assured a 3.75% return, and the validator maintains the CESR performance standard.

As a result, unlike the current scenario, the client consistently receives 0.9375 ETH every quarter.

Example 2

While it seems a winning scenario for the validator, it can also not be so - in a case where a validator makes just enough to meet the CESR. In this situation, the validator fails to make a commission, but the client's interest is protected and they will receive their fixed rate as usual.

These are hypothetical situations but can pan out in real life as well. In a practical scenario, a trusted validator like Luganodes always has 365 x 24 x 7 uptime to ensure that the reward rate always stays high above a threshold. CESR is a validator-wide threshold that validators can now abide by.

Validators thus benefit from CESR as they can dictate commission rates based on their confidence in their performance and provide stable revenue to clients.

Liquidity Providers

Now, let's shine some extra light on Liquidity Providers who actually make the whole arrangement possible. As mentioned earlier, they use the CESR arrangement with validators as a hedge and as a speculative derivative. Let’s use another example from traditional industries to demonstrate this.

Hedge

LPs seek a benchmark rate that validators should adhere to. For example, an airline company hedges fuel costs by agreeing to a fixed rate, regardless of market fluctuations.

In an airline company, fuel is a major expense; thus it is not uncommon for airlines to have deals in place with a petroleum company to buy exclusively from them. In such arrangements airlines often pay above market price - but at a fixed rate. The fixed rate remains valid even when fuel prices fluctuate or rise sharply.

Fuel consumption per Quarter = 100 Litres

An example of hedge for an Airline company

| Fuel Cost in Rs (per liter) | Total Cost | Fixed Rate (monthly) | |

|---|---|---|---|

| Q1 | 100 | 10000 | 11000 |

| Q2 | 80 | 8000 | 11000 |

| Q3 | 90 | 9000 | 11000 |

| Q4 | 170 | 17000 | 11000 |

Similarly, liquidity providers have a certain set of customers, such as Web3 protocols (L1,L2s, Defi protocols) and exchanges. These companies require a regular supply of gas fees for their operations.

| Gas Fee (monthly) | Fixed Rate | Rewards from Staking | |

|---|---|---|---|

| Q1 | 10 | 15 | 9 |

| Q2 | 13 | 15 | 11 |

| Q3 | 11 | 15 | 10 |

| Q4 | 30 | 15 | 25 |

By signing up for CESR, Liquidity Providers act as fuel providers which provide gas fees to these companies at a fixed rate. Meanwhile, LPs leverage

Exchanges and other ventures receive their required gas fees from LPs at a fixed rate. In the event that gas fees sharply rise, LPs still have to provide the required tokens at the fixed rate, potentially incurring a loss. An increase in gas fees may lead to an increase in validator rewards, although this relationship is not direct, as staking rewards are influenced by multiple factors. However, having a hedge helps. By participating in the CESR agreement, LPs can use rewards from staking to balance out their losses.

Speculative Derivative

In traditional finance, speculative derivatives are everywhere. There are many products that rely on speculating on a particular price and moving funds to create profits. The same is now being reflected in cryptocurrencies. Liquidity provider fund managers can enter these swaps if they believe the CESR (or Ethereum reward rate) will increase. By having funds allocated to staking, they can take an early piece of the pie, when staking rates inflate in the future.

Comparison to LIBOR

Taking another leaf out of traditional finance, we discuss LIBOR, which in essence is quite similar to CESR.

LIBOR, or the London Interbank Offered Rate, was a benchmark interest rate used by major global banks to lend to one another, influencing a wide range of financial products like loans and mortgages. However, LIBOR faced significant issues, including manipulation and lack of transparency, which ultimately led to its replacement by more reliable benchmarks such as the Secured Overnight Financing Rate (SOFR).

Similarly, CESR, or the Composite Ether Staking Rate, acts as a benchmark rate within the cryptocurrency market. Just as LIBOR provided a stable reference point for interest rates in traditional finance, CESR offers a stable and predictable return rate for staking participants in the blockchain space.

The key difference is that CESR benefits from the lessons learned from LIBOR's shortcomings. Knowing that these issues have been identified and corrected in traditional finance, CESR is designed to avoid similar problems. On the other hand, CESR is more transparent, as anyone can calculate CESR and cross-verify it using data available on the blockchain. This transparency ensures that CESR can deliver reliable and verifiable returns, bringing a tried-and-true financial concept from traditional finance (TradFi) into the world of decentralized finance (DeFi) with improved safeguards.

Conclusion

CESR therefore, introduces a stable and predictable financial structure for clients, validators, and liquidity providers alike. This implementation is a novel concept for Web3 and the ecosystem can certainly profit from such an agreement. As a mainstay in the institutional staking industry, Luganodes is excited to participate in CESR and bring more to the table. More announcements and explainers to follow, stay tuned!

About Luganodes

Luganodes is a world-class, non-custodial blockchain infrastructure provider that has rapidly gained recognition in the industry for offering institutional-grade services. It was born out of the Lugano Plan B Program, an initiative driven by Tether and the City of Lugano. Luganodes maintains an exceptional 99.9% uptime with round-the-clock monitoring by SRE experts. With support for 40+ PoS networks and serving 60+ institutional cliens, it ranks among the top validators on Polygon, Polkadot, Sui, and Tron. Luganodes prioritizes security and compliance, holding the distinction of being one of the first staking providers to adhere to all SOC 2 Type II, GDPR, and ISO 27001 standards as well as offering Chainproof insurance to institutional clients.

The information herein is for general informational purposes only and does not constitute legal, business, tax, professional, financial, or investment advice. No warranties are made regarding its accuracy, correctness, completeness, or reliability. Luganodes and its affiliates disclaim all liability for any losses or damages arising from reliance on this information. Luganodes is not obligated to update or amend any content. Use at your own risk. For specific guidance, please consult a qualified professional.